Cheap Car Insurance in Georgia With No Deposit

Georgia No Deposit Car Insurance

Samantha Johnson

— insurance policy expert

Every driver in Georgia needs car insurance, but for many households, the hardest part isn’t the monthly bill; it’s the upfront chunk of money required to activate a policy. Ads promising “no down payment car insurance in GA” sound appealing, but what does that really mean in Georgia? This guide dives deep into the facts, explains how payment structures work, and shows you where to find the cheapest options to get covered without draining your wallet.

We’ll go into depth on:

- Georgia’s insurance requirements and how the law shapes upfront payments.

- The top five companies with low-start policies.

- Payment plans and deductible strategies.

- How location affects your rate.

- Hidden costs, scams to avoid, and real-world examples.

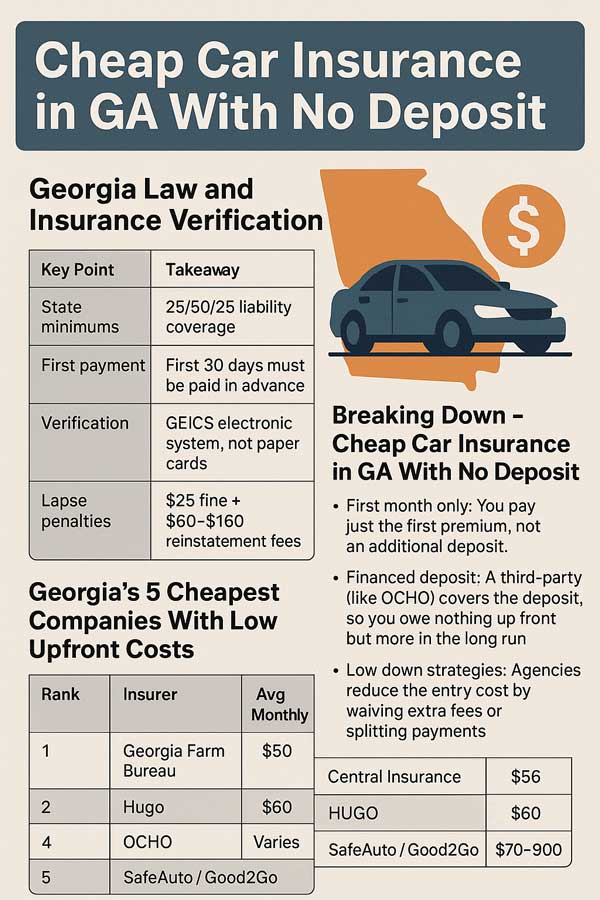

Georgia Law and Insurance Verification

Before you can register or renew your tags in Georgia, proof of insurance must be on file with the Georgia Electronic Insurance Compliance System (GEICS). Insurance cards in your wallet aren’t enough if GEICS shows a lapse.

By law, companies cannot issue a policy without collecting the first 30 days of premium. This rule makes “first month free” coverage impossible, no matter what a TV ad might say.

Quick Snapshot

| Key Point | Takeaway |

| State minimums | 25/50/25 liability coverage |

| First payment | First 30 days must be paid in advance |

| Verification | GEICS electronic system, not paper cards |

| Lapse penalties | $25 fine + $60–$160 reinstatement fees |

| “No down payment” | Usually means the first month only, or a financed deposit |

Breaking Down – Cheap Car Insurance in GA With No Deposit

When you see “cheap car insurance with $0 down” ads in Georgia, it might sound too good to be true. Here’s what’s really going on:

- First month only: You pay just the first premium, not an additional deposit.

- Financed deposit: A third-party (like OCHO) covers the deposit, so you owe nothing up front but more in the long run.

- Low down strategies: Agencies reduce the entry cost by waiving extra fees or splitting payments.

The key: you always owe at least the first month. Anything else is marketing language.

Georgia’s 5 Cheapest Companies With Low Upfront Costs

| Rank | Insurer | Avg Monthly | Why It Works |

| 1 | Georgia Farm Bureau | $50 | Local focus, minimal start costs |

| 2 | Central Insurance | $56 | Low liability rates for clean drivers |

| 3 | Hugo | $60 | Pay-as-you-go micro-payments, $0 start options |

| 4 | OCHO | Varies | Finances deposits, true $0 today availability |

| 5 | SafeAuto / Good2Go | $70–$90 | Non-standard carriers, flexible starts for high-risk drivers |

Pro Tip: In Georgia, compare insurers that let you backdate your policy start date by a few days. This trick keeps your coverage continuous in GEICS, avoids costly lapse penalties, and can save you more than chasing a $0-down plan.

Georgia Farm Bureau: Cheapest Liability Rates

Farm Bureau offers the lowest average monthly bill for drivers seeking liability-only coverage:

- Liability-only: About $50 per month.

- Full coverage: Around $122 per month.

Their local underwriting and discount programs help keep costs low for Georgia residents, with payment schedules that minimize what you owe up front.

Strategies to Lower Your First Payment

- Choose liability-only if your vehicle is paid off.

- Get quotes from multiple companies (rates swing widely by ZIP code).

- Stack discounts like autopay, bundling, and safe driver perks.

- Raise your deductible for lower monthly bills.

- Use financing options only when you truly need to.

- Never let your policy lapse—it costs more to reinstate than any deposit savings.

Deductibles and Their Impact

| Deductible | Avg Monthly Bill |

| $250 | $110 |

| $500 | $90 |

| $1,000 | $70 |

A higher deductible means a lower premium. If you can afford the risk, it’s one of the most reliable ways to shrink both upfront and long-term costs.

Lapse Penalties in Georgia

| Offense | Fine | Reinstatement Fee | Total |

| First | $25 | $60 | $85 |

| Second | $25 | $60 | $85 |

| Third+ | $25 | $160 | $185 |

A lapse costs more than any deposit savings. Continuous coverage is always cheaper.

10 Discounts to Save Money on Georgia Car Insurance

- Safe Driver Discount – Stay accident- and violation-free for 3–5 years, and insurers like State Farm, Farm Bureau, and Progressive will reward you.

- Multi-Policy Discount – Bundle auto with homeowners, renters, or life insurance for savings of 10–25%.

- Good Student Discount – Drivers under 25 with a GPA of 3.0+ or Dean’s List honors get lower premiums.

- Defensive Driving Course Discount – Approved courses in Georgia can shave 10–15% off liability premiums.

- Vehicle Safety Features Discount – Cars equipped with anti-theft systems, airbags, or anti-lock brakes qualify for lower rates.

- Low-Mileage Discount – If you drive fewer than 7,500 miles annually, ask about a low-mileage credit.

- Usage-Based / Telematics Discount – Programs like Progressive’s Snapshot or Allstate’s Drivewise reward safe habits such as gentle braking and low nighttime driving.

- Autopay and Paperless Billing Discount – Many carriers in Georgia (Farm Bureau, Central, and national brands) cut $5–$10 monthly for setting up autopay and going paperless.

- Multi-Car Discount – Insure more than one car under the same household policy and save up to 25%.

- Membership or Affiliation Discount – Certain groups (teachers, military, alumni associations) get special preferred rates in Georgia.

Real Life Georgia Auto Insurance Rate Examples

Atlanta Student: A 21-year-old shaved her first payment from $220 to $155 by choosing Hugo with a $1,000 deductible, plus discounts for autopay and paperless billing.

Albany Retiree: At 65, Robert picked semi-annual Farm Bureau coverage. Paying $880 up front saved him $140 over the year compared to monthly installments.

FAQs

Can I get $0 down insurance?

Not unless you use financing or pay-as-you-go platforms.

Do police accept paper proof?

No—GEICS electronic verification is what matters.

What if I miss a payment?

Some insurers allow grace periods, but reinstatement costs more than deposits.

What are the minimums in Georgia?

25/50/25 liability coverage.

Do deductibles help with upfront costs?

Yes, higher deductibles bring lower premiums immediately.

Do SR-22 filings change things?

Yes, they increase premiums and usually block $0 down options.

The Final Word On Cheap Car Insurance In GA With No Down Payment

Georgia law requires 30 days prepaid, so there’s no loophole for truly free coverage. Still, smart drivers can keep upfront costs low by choosing liability-only coverage, raising deductibles, using discounts, and considering deposit financing when necessary. Local carriers like Farm Bureau and Central Insurance, plus flexible newcomers like Hugo and OCHO, make it possible to get insured today without emptying your wallet.

The bottom line: not all insurers in GA offer cheap auto insurance with no down payment. One of the smartest moves you can make is to structure your policy to balance affordability, protection, and compliance.

Get up to ten auto insurance quotes in about five minutes and save hundreds. See how easy it is to save on cheap Georgia car insurance with direct rates.