General Liability Car Insurance

Protection for life's unexpected turns

The Backbone of Your Policy: Paying Others’ Bills and Shielding Your Assets Beyond State Minimums

General liability car insurance is the backbone of every auto policy and one of the most important forms of financial protection a driver can carry. It pays for injuries, property damage, and legal costs if you cause an accident that harms others. Without it, one mistake behind the wheel could turn into years of financial hardship. Though many people associate the term “general liability” with business insurance, in the context of auto coverage, it refers to the section of your policy that shields your assets and income when you are found at fault in a crash.

Liability insurance ensures that victims of an accident receive compensation for their losses while protecting you from devastating lawsuits. Even a small collision can trigger hospital bills, vehicle repairs, and lost wages that easily exceed state minimum requirements. By carrying enough coverage, you are not just following the law; you are protecting your financial future.

Understanding Liability Coverage

Liability insurance consists of two parts: bodily injury and property damage. Bodily injury covers the medical care, rehabilitation, and lost wages of others when you are at fault. Property damage covers the cost of repairing or replacing vehicles, fences, buildings, or other property you damage in a crash. It does not pay for your own injuries or vehicle repairs.

Every policy includes limits, which are the maximum amounts the insurer will pay for each type of loss. These are often expressed as three figures: one for each person injured, one for all injuries per accident, and one for property damage. Some insurers offer a combined single limit that merges these amounts into one overall pool of protection.

Because the cost of medical treatment and vehicle repair has risen sharply, experts recommend carrying higher limits than the minimum required by law. Many drivers choose at least $100,000 per person, $300,000 per accident, and $100,000 for property damage, or they select a combined single limit policy that provides the same level of protection in a simpler format.

Beyond paying bills, liability insurance also provides legal defense. If you are sued, your insurer will hire and pay attorneys to represent you up to the limits of your policy. This protection alone can save you tens of thousands of dollars in legal costs and is one of the most valuable features of the coverage

Choosing the Right Amount of Coverage

Selecting your coverage limits depends on what you have to protect. If you own a home, have savings, or earn a substantial income, it makes sense to carry higher limits. A court judgment can reach your assets and even future earnings if your coverage runs out. For most middle-income households, $100,000 per person and $300,000 per accident provide strong protection. Higher earners often increase those limits and add a personal umbrella policy that extends protection by an additional one or two million dollars at a relatively low cost.

Urban drivers face special risks. Collisions in congested areas often involve multiple vehicles and expensive property damage. Rural drivers encounter high-speed crashes that can cause severe injuries. In either case, higher limits are an affordable safeguard compared with the potential cost of being underinsured. The goal is to buy enough liability insurance so that your insurer, not you, pays for nearly every realistic claim scenario.

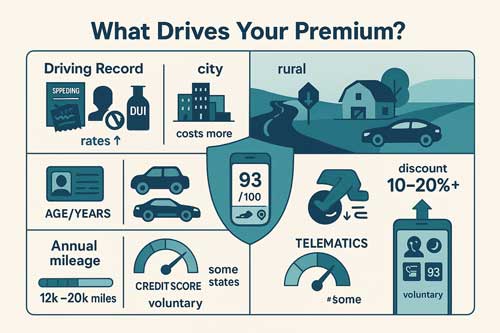

What Determines the Cost of Liability Auto Insurance

Premiums vary widely based on several key factors. Your driving record is the most important factor. Tickets, accidents, and DUI convictions can dramatically increase your rates. Where you live also matters. City drivers pay more than rural drivers because dense traffic leads to more claims. Age, gender, and years of driving experience play roles as well, since new and very young drivers statistically have more accidents.

The vehicle you drive affects your premium because certain cars cost more to repair or are involved in more frequent claims. Annual mileage is another consideration; the more you drive, the greater the risk exposure. In some states, insurers use credit-based scores to predict claim likelihood, so maintaining good credit can lower your rates.

Telematics programs have added a new way to save. These apps or devices track your driving habits and reward safe, low-risk behavior, such as avoiding hard braking and speeding. Drivers who score well can earn discounts of ten to twenty percent or more. Because these programs are voluntary, you can test them without obligation and see whether your habits translate into savings.

The Cheapest Insurers For Liability Auto Insurance Coverage

While rates depend on the state and driver profile, several insurers consistently offer affordable liability coverage. GEICO frequently ranks among the least expensive for drivers with clean records who prefer to manage their policies online. State Farm remains a favorite for its balance of competitive pricing, local agents, and strong multi-policy discounts. Progressive appeals to a wide range of drivers, offering flexibility for those with both perfect and less-than-perfect histories, plus solid telematics savings through its Snapshot program. Nationwide often delivers competitive bundle discounts for homeowners and multi-vehicle households, while Travelers attracts customers who prefer stable pricing and options for higher liability limits.

Regional carriers can also be strong contenders. Many state-based or farm bureau insurers price aggressively within their territories. Comparing at least five carriers on the same day with identical coverage limits ensures you get a fair market view of current rates.

Liability Insurance for Teens and Seniors

Teen drivers present the highest risk category, making their premiums expensive. The best strategy is to keep them on a family policy rather than buying a separate one. This allows them to share discounts for multi-car coverage and bundling. Safe, modest vehicles with strong crash-test ratings and driver-assistance features help reduce premiums. Enrolling teens in telematics programs not only promotes safe habits but can lower rates after a few months of good data. Submitting proof of driver education courses and good grades usually leads to additional savings. With each claim-free year, rates decline significantly.

Seniors benefit from experience but may face rate increases as insurers consider slower reaction times and potential health issues. Taking a state-approved mature driver course can cut costs, and verifying low annual mileage ensures proper classification in a cheaper rate tier. Choosing cars with modern safety technology and maintaining a good credit record further helps control expenses. Bundling home and auto policies or paying in full for the policy term can also offset age-related pricing differences.

Discounts That Matter The Most

Although insurers advertise many discounts, a few deliver the greatest savings. Bundling auto with home or renters coverage often reduces costs dramatically. Maintaining a clean driving record over several years results in a strong safe-driver discount. Telematics or usage-based programs reward careful drivers and are especially effective for commuters who rarely drive at night.

Paying the premium in full instead of monthly avoids service fees and may qualify for a small reduction. Enrolling in automatic payments and going paperless adds minor savings that stack up. Taking defensive driving courses benefits both young and older drivers, while students with strong academic performance typically qualify for good-student discounts. Low-mileage ratings and membership affiliations, such as alumni or professional groups, can also lower costs. The key is to combine multiple discounts for maximum impact and to confirm with your insurer how each one applies.

How to Shop for General Liability Auto Insurance Coverage

Finding the best rate is about consistency and comparison. Start by choosing your desired coverage limit, then gather information about each driver and vehicle in your household. Obtain quotes from several companies on the same day using identical data so that rate differences reflect real competition rather than timing. Ask about telematics, bundling opportunities, and any state-specific credits. Review each quote carefully to ensure the limits, deductibles, and discounts are listed correctly before purchasing.

Revisit your policy once or twice a year, particularly when life changes occur, such as moving, buying a new car, or when tickets or accidents drop off your record. Because insurance markets fluctuate, regularly shopping for your coverage keeps premiums in check. Treat your policy as a living document that can evolve with your needs rather than a set-and-forget expense.

Frequently Asked Questions

Many drivers wonder what liability insurance actually covers.

It pays for other people’s injuries, property damage, and your legal defense when you are at fault in a crash. It does not cover your own car or medical bills; you need collision or medical payments coverage for that.

Policy limits can be confusing.

When a policy lists something like 100/300/100, it means up to $100,000 for one person’s injuries, $300,000 for all injuries in a single accident, and $100,000 for property damage. Some prefer a single combined limit, which offers more flexibility.

Small claims may raise your rate if you are at fault, so discuss potential impacts with your agent before filing.

Uninsured motorist coverage, which pays for your injuries if the other driver lacks insurance, is a wise companion to liability insurance. Telematics programs can save money if you drive safely and maintain consistent habits. Drivers can also choose liability-only coverage for older vehicles that no longer justify full coverage, as long as state law permits it.

Experts recommend reviewing and comparing policies annually or after significant life changes.

Regular attention to your policy ensures your coverage and costs stay balanced and competitive.

The Final Word On General Liability Car Insurance

General liability car insurance is more than a legal requirement—it is a financial safety net that preserves your security and peace of mind every time you drive. It covers the costs you owe others, pays for your legal defense, and protects your assets from lawsuits that could otherwise devastate your finances. The best approach combines thoughtful coverage limits, active discount management, and periodic re-shopping to ensure you always have strong protection at the best price.

Whether you are a new driver, a parent insuring a teenager, or a retiree looking to simplify expenses, liability coverage remains the most essential part of your auto policy. In an unpredictable world, where one mistake can lead to immense costs, carrying robust general liability car insurance is not just wise, it’s the foundation of responsible driving and financial stability. Get your custom general liability car insurance quote in about five minutes. Save hundreds with direct liability coverage.