Zero Down Car Insurance Plans

Last updated on February 5, 2026

The Generalinsurance.org Editorial Team produces informational content about insurance topics, focusing on clear, practical explanations to help readers understand common coverage options, costs, and shopping considerations.

Articles cover everyday questions related to auto, home, renters, life, and other insurance categories, including policy basics, pricing factors, coverage comparisons, and ways consumers may reduce costs while maintaining appropriate protection.

Content reviewed internally for clarity and consistency of general insurance concepts.

Note: This content is for general informational purposes only and does not constitute insurance, legal, or financial advice. Generalinsurance.org is an independent informational website and is not affiliated with any insurer.

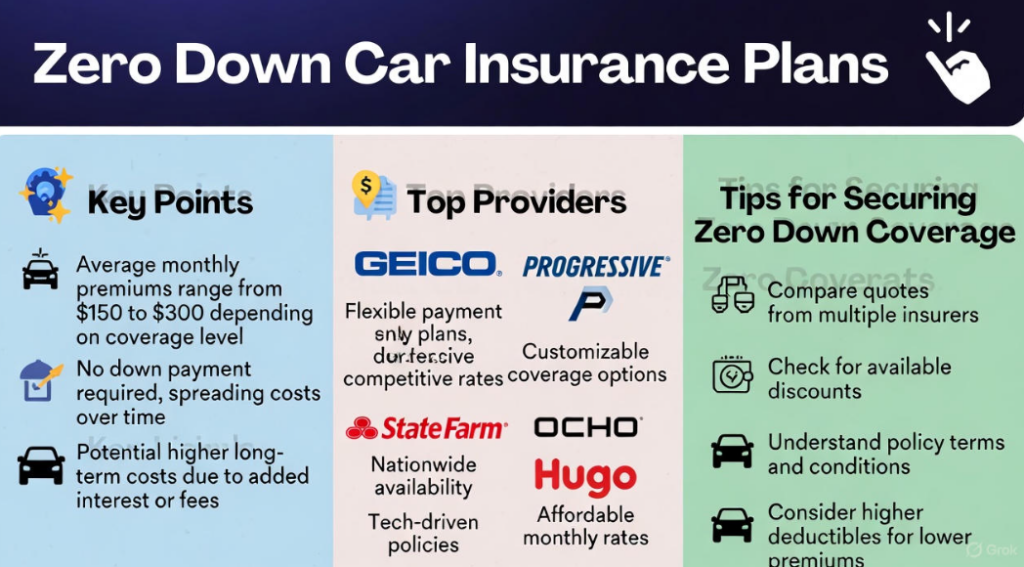

Low upfront car insurance, often marketed as “zero down” coverage, is one of the most appealing options for drivers facing tight budgets. In reality, true $0 upfront coverage from reputable insurers doesn’t exist; all legitimate policies require at least the first month’s premium to activate. However, many companies offer flexible plans that minimize the initial payment, sometimes through financing or short-term options, making coverage more accessible without requiring a large lump sum.

This approach helps drivers avoid lapses, meet state requirements, or register a vehicle quickly. With national average full coverage premiums around $2,697 annually (or $225 monthly) as of 2026, spreading costs via monthly billing can ease cash flow – though it may add small installment fees. Innovative providers like OCHO and Hugo are changing the game by offering genuine low- or no-deposit structures, often with interest-free financing or pay-as-you-go models.

Understanding eligibility, costs, and providers is key to securing protection without financial strain. If you want a simple foundation before comparing companies, start with Car Insurance Basics.

The Reality of “Zero Down” Auto Insurance Policies

The term “zero down” is often a misleading marketing tactic. Legitimate insurers require payment before coverage begins to mitigate risk – no policy activates for free. What companies advertise as “zero down” typically means:

- Your first month’s premium serves as the “deposit.”

- No additional upfront lump sum (e.g., 20-30% of the annual premium) beyond that.

- Coverage starts immediately after the initial payment.

For example, on a $1,200 annual policy, traditional plans might require $200-300 upfront. Low-upfront options let you pay just the prorated first month (around $100) and bill the rest monthly.

True innovations exist: OCHO finances the insurer’s required deposit interest-free (0% APR), allowing qualified drivers to start with $0 out-of-pocket while repaying in paycheck-aligned installments. Hugo offers pay-as-you-go with no upfront fees beyond a minimal initial load (e.g., 3-7 days’ coverage).

These structures are legal nationwide but vary by state regulations and insurer availability. Beware scams promising completely free starts—they’re red flags.

How No Down Payment Plans Work And Cost

Car insurance payment plans fall into categories:

- Pay-in-full: Often a 5-15% discount, but requires full annual premium upfront.

- Installment (monthly/semi-annual): Most common for low upfront; adds $3-10 processing fees per bill, increasing total cost slightly (e.g., $36-120/year extra).

- Financed low-upfront: Providers like OCHO cover the deposit, you repay interest-free.

- Pay-as-you-go: Hugo charges per day/week used, ideal for infrequent drivers.

Average upfront costs in 2026:

- Minimum coverage: $40-70 (first month for clean drivers).

- Full coverage: $150-250.

- High-risk (DUI/accidents): Often higher deposits.

Monthly plans cost more overall due to fees, but preserve cash flow. Paying upfront or semi-annually saves most long-term. To see what different carriers actually charge and how payment plans change the first bill, use Compare Auto Insurance Quotes.

Things To Consider When Searching For Zero Down Car Insurance

At its core, zero down car insurance refers to auto policies that eliminate or drastically reduce the initial lump-sum payment required to activate coverage. In standard insurance setups, companies often mandate a deposit to cover potential early cancellations or administrative costs. For instance, on a $1,500 annual policy, you might need to pay $300-$450 upfront, with the remainder spread over monthly installments.

Zero down flips this model by letting you pay only the prorated first month’s premium—often as low as $40-$100 for minimum coverage, to bind the policy. Coverage kicks in immediately, and subsequent payments are handled via automatic withdrawals, credit cards, or even paycheck deductions for added flexibility. If you’re deciding between liability-only and fuller protection, this guide on Minimum Coverage Car Insurance helps you compare what you actually get.

But not all “zero down” claims are equal. Many advertisements from big-name insurers like GEICO or Progressive actually mean “no additional deposit beyond the first installment,” which still requires some money up front. True zero down, where you pay nothing at activation, is rarer and typically offered through specialized platforms like OCHO, which finances the initial premium at 0% interest. This financing is essentially a short-term loan repaid over the policy term, often aligned with your pay schedule to avoid cash flow issues.

Key differences from traditional policies include:

- Payment Structure: Traditional plans favor pay-in-full or semi-annual options with discounts (5-15% savings), while zero down emphasizes monthly or bi-weekly billing, potentially adding small fees ($3-10 per payment).

- Risk Assessment: Insurers use credit checks, driving history, and telematics data to approve low-upfront plans, as they assume higher cancellation risks.

- Coverage Types: Zero down is available for liability-only (cheapest and easiest to get), full coverage (including collision and comprehensive), and even add-ons like roadside assistance, but eligibility tightens for higher-risk profiles.

Pros of zero down include immediate accessibility, better budgeting for variable incomes, and the ability to avoid coverage lapses that could hike future rates by 20-50%. Cons? Slightly higher overall costs due to installment fees and forfeited pay-in-full discounts. In real-world terms, a driver in Texas with a clean record might pay $50 upfront for zero down minimum coverage versus $200 for a traditional plan, but it’s important to note the annual total could be $50 more with fees.

It’s worth noting that zero down isn’t “free insurance”; you’ll always owe the full premium eventually. Scams promising no payments at all are rampant online; always check for state licensing and Better Business Bureau ratings.

Top Providers for Zero Down Car Insurance

Major insurers and innovators lead flexible plans:

- GEICO: Often the cheapest base rates (~$43/month minimum); many qualify for a first-month-only start.

- Progressive: Flexible for high-risk; low deposits are common.

- State Farm: Reliable monthly billing; good for bundling discounts.

- OCHO: Stands out with genuine $0 down via 0% financing; partners with carriers for competitive rates; builds credit with on-time payments.

- Hugo: True pay-as-you-go (3+ days); no deposit beyond initial load; pause when not driving—great for gig/low-mileage drivers.

Other notables: USAA (military-eligible, low rates); Nationwide (usage-based savings).

Metromile’s pay-per-mile model (acquired by Lemonade) offers low burdens for infrequent drivers but no longer accepts new standalone policies. Compare at least 4-5 quotes as rates vary widely. If you need coverage to start immediately after payment, check Instant Auto Insurance Quote options that can bind same day.

Smart Options For High-Risk Drivers and SR-22 Filings

High-risk drivers (DUIs, accidents, lapses) face steeper premiums and stricter deposits, but low-upfront options exist.

SR-22 (certificate proving coverage) is often required—adds $20-50 filing fee, but not a separate policy.

Providers accommodating SR-22 with flexible payments:

- Progressive & The General: Specialize in high-risk, often monthly plans.

- OCHO/Hugo: May support depending on state/underwriter.

- State Farm/GEICO: Possible but higher scrutiny.

Smart Tip: Choose minimum coverage initially; then improve your driving record for future savings. Lapses restart SR-22 clocks, so make sure to maintain continuous coverage.

Frequently Asked Questions About Zero Down Auto Insurance

- Is true zero-down car insurance possible? Rarely from traditional insurers, OCHO offers the closest via financing.

- Does monthly billing cost more? Yes, slightly due to fees; pay-in-full saves most.

- Best for bad credit/high-risk? Progressive, OCHO, or non-standard carriers.

- Can I get full coverage low-upfront? Yes, but harder/more expensive than liability-only.

- How fast can coverage start? Same day with online providers after initial payment.

The Final Word On Zero Down Car Insurance

Low upfront car insurance makes protection realistic without draining savings. While no free options exist, flexible plans from GEICO, Progressive, OCHO, and Hugo minimize barriers—often starting coverage for under $50 initially.

Compare quotes, prioritize continuous coverage to avoid rate hikes, and consider needs (minimum vs. full). Responsible choices lead to lower long-term costs and peace of mind.

Shop smart and compare zero down car insurance plans in under five minutes. Get cheaper auto insurance with direct rates online. To jump straight into pricing, start here: General Insurance Quotes.