How Much Is General Car Insurance?

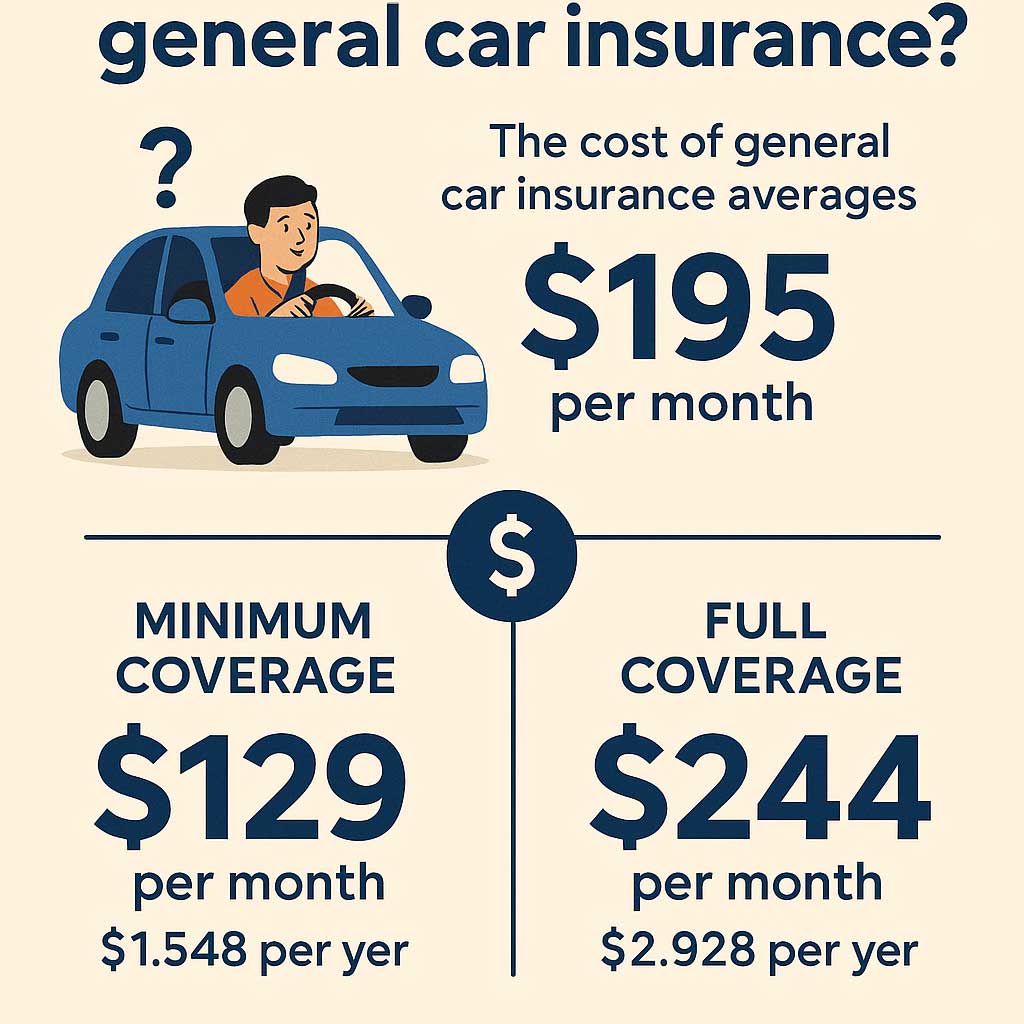

Many drivers searching for the best and cheapest coverage often ask: How much is general car insurance? The cost of general auto insurance matters more than anything else when choosing a policy. The cost of general insurance averages $195 per month nationwide or $2,340 per year.

For minimum coverage, a general insurance policy averages $129 per month or $1,548 per year, and full coverage averages $244 per month and $2,928 annually. General auto insurance rates will vary based on many factors, including the vehicle insured and the driver’s zip code. While national averages provide a starting point, your personal situation is what truly determines your general insurance rate.

National Average Cost of General Auto Insurance

To determine what most drivers typically pay, let’s begin with national averages for general car insurance. A full-coverage policy for the average driver generally costs a little more than two thousand dollars per year. This usually breaks down to somewhere below two hundred dollars per month. Drivers who select minimum liability, which meets only the legal requirements of their state, often pay significantly less, sometimes under one thousand dollars per year.

Minimum liability is cheaper because it provides only basic financial protection for other people’s injuries and property. It does not protect your own vehicle. Full coverage includes liability, collision, and comprehensive protection, which significantly increases the value of the policy and the total annual cost.

These averages assume a standard driver: mid-aged, clean driving record, typical vehicle, and average commuter mileage. Your personal rate can be higher or lower depending on risk factors that insurers measure. Even though averages give you a baseline, they are not a guarantee of your cost. They simply help you understand what the typical driver pays before individual variables come into play.

Why Your General Car Insurance Rate May Be Higher or Lower

General car insurance premiums are based entirely on risk. The greater the insurer believes your chances are of filing a claim, the more your premium will be. Below are the most important factors that influence your rate.

Driving Record

A clean driving record with no accidents or violations usually results in the lowest rates available. Any at-fault accident, ticket, or claim can increase your premium dramatically. Insurers evaluate your history over several years, so even older violations can still affect your price.

Credit Profile

Many insurers use credit-based insurance scoring as a predictor of risk. Drivers with a higher credit score often pay lower premiums. Those with lower credit scores may pay more. While not all states allow credit scoring in auto insurance, many still do.

Location

Your ZIP code matters. Urban areas with high traffic density, accident frequency, theft rates, and repair costs typically have higher insurance premiums. Rural areas with lower risk trends generally offer lower premiums. Your state’s insurance laws also influence what you pay.

Vehicle Type

The make and model of your car significantly impact your premium. Vehicles with expensive repair costs, high theft rates, or powerful engines typically cost more to insure. Safe vehicles with strong crash-test ratings, affordable parts, and lower theft risk tend to cost less.

Coverage Level and Deductible

Minimum liability coverage is always cheaper than full coverage because you’re insuring less. A higher deductible lowers your rate, while a lower deductible raises it. Collision and comprehensive coverage add to your total cost.

Age and Gender

Younger drivers, particularly teenagers, pay the highest premiums. They lack experience and have statistically higher accident rates. Mature drivers generally pay less. Seniors may see their rates increase depending on the insurer and their driving profile.

Mileage and Vehicle Usage

Long-distance commuters often pay more than drivers who log fewer miles. The more time you spend on the road, the more likely you are to be involved in an accident.

Marital Status

Insurers often give married drivers slightly lower premiums because data shows they file fewer claims.

All these factors interact to determine your rate. A single high-risk factor may not drastically increase your premium, but multiple risk indicators combined can make your policy much more expensive.

Average General Auto Insurance Rates By Driver Profile and Location

To better understand what general car insurance costs, it helps to consider how different factors apply to real-world driver profiles. The following examples help highlight how premiums shift for different groups.

Sample Monthly Costs by Driver Profile (National Averages)

| Driver profile | Typical monthly cost (full coverage) | Approx. annual cost | Why it costs this much |

|---|---|---|---|

| Clean adult driver (good credit) | $120–$215 | $1,440–$2,580 | Lowest average rates; good credit and clean record signal lower risk to insurers. |

| Young driver (ages 19–25) | ≈ $537 | ≈ $6,444 | Young drivers have the highest claim frequency, so insurers charge much higher premiums. |

| Driver with recent DUI | ≈ $377 | ≈ $4,524 | A DUI is one of the strongest risk signals and can more than double the cost in some markets. |

| Driver with poor credit | ≈ $313 | ≈ $3,756 | In most states, poor credit is linked to more frequent claims, so premiums increase. |

| Driver with at-fault accident | ≈ $310 | ≈ $3,720 | Recent at-fault accidents suggest a higher chance of future losses for the insurer. |

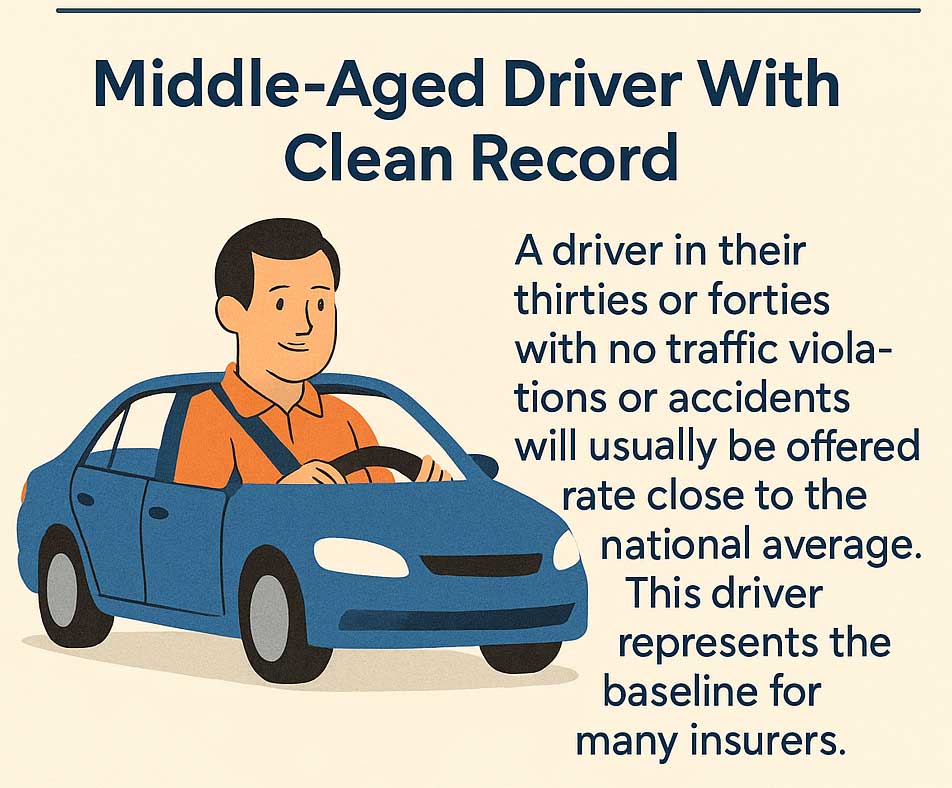

Middle-Aged Driver With Clean Record

A driver in their thirties or forties with no traffic violations or accidents will usually be offered a rate close to the national average. This driver represents the baseline for many insurers.

Driver in an Accident

One at-fault accident can noticeably increase premiums. Two or more accidents often cause rates to climb sharply. Some insurers offer accident forgiveness, but not all do.

Teen Driver

Teenagers are the most expensive group to insure because they have limited driving experience and higher accident statistics. Adding a teen to a policy can increase the total household premium significantly.

Senior Driver

Rates for senior drivers vary. Some insurers raise premiums for older drivers if their risk profile shows an increased likelihood of claims.

By State and Region

Certain states typically have higher premiums because of dense traffic, higher repair costs, weather patterns, or legal frameworks. If you live in an area known for high claim frequency or expensive repairs, expect to pay more regardless of driving experience.

Sample Premium Ranges

Clean-record drivers might pay under a thousand dollars for minimum coverage or a little more than two thousand for full coverage. High-risk drivers may pay several thousand dollars per year. These variations show why personalized quotes are necessary.

Understanding Monthly Payments And How General Automobile Insurance Premiums Are Structured

Although auto insurance is priced annually, monthly payments are far more common. Monthly billing is convenient, but it may increase the total amount you pay due to installment fees. When you choose monthly payments, your insurer divides your annual premium into twelve payments and may add a small processing fee each month.

This means a full-coverage policy costing a little more than two thousand dollars annually may cost slightly more when paid monthly. Some insurers waive monthly fees if you enable automatic payments or use electronic billing.

Paying annually or semiannually is almost always cheaper. If you can afford a larger upfront payment, you may save money over the long term.

How to Estimate Your Own General Car Insurance Cost

Estimating your personal premium is straightforward when you follow the steps insurers use to price your policy.

Gather Your Information

Have your vehicle details, driver’s license, mileage, and address available so you can receive accurate estimates.

Review Your Driving History

Accidents, violations, and claims impact your price. Knowing what’s on your record helps set realistic expectations.

Understand Your Credit Profile

If your state allows credit scoring, your credit score can influence your premium. Knowing your score beforehand helps you evaluate quotes.

Choose Your Coverage Level

Decide whether you want minimum liability, full coverage, or a mix of both. Your choice heavily affects your final premium.

Get Multiple Quotes

Every insurer weighs risks differently. A driver could receive very different prices from three companies even with identical information. Always compare at least three quotes.

Apply Discounts

Discounts can help lower premiums significantly. Many drivers qualify for more discounts than they realize.

Use Online Tools

Cost estimators and insurance calculators can give you ballpark numbers before you begin comparing quotes.

Following these steps helps you create a close estimate of your likely premium before you officially apply.

Ten Proven Ways to Lower Your General Car Insurance Rate

Most drivers want the lowest rate possible without losing important coverage. Here are ten proven strategies you can use.

Improve Your Driving Record

Safe driving lowers your risk and your premium. Avoiding tickets and accidents is the most effective long-term cost-saving strategy.

Raise Your Deductible

Choosing a higher deductible reduces your monthly premium because you are taking on more financial responsibility in the event of a claim.

Remove Unnecessary Coverage From Older Cars

If your vehicle is older and its value has declined, consider dropping collision or comprehensive coverage.

Bundle Insurance Policies

When you combine auto insurance with homeowners or renters insurance, many insurers offer significant discounts.

Take Advantage of Discounts

Common discounts include safe driver, good student, multi-car, loyalty, and safety equipment discounts. Even a few small discounts can noticeably reduce your total cost.

Reduce Annual Mileage

If you can adjust your commute or use your vehicle less often, you may qualify for low-mileage discounts.

Choose a Safer Vehicle

Cars with lower repair costs, better safety ratings, and fewer theft claims cost less to insure.

Improve Your Credit

Better credit often results in lower insurance premiums in states where credit scoring is allowed.

Shop Around Regularly

Insurance rates change often. Comparing quotes once a year ensures you don’t overpay.

Add Security or Anti-Theft Features

Features like alarms, tracking systems, and immobilizers help deter theft and may lower your premium.

Frequently Asked Questions About General Car Insurance Plans

Why did my premium go up even without any accidents?

Premiums can change due to inflation, increased local claims, higher repair costs, or insurer-wide adjustments, even when your driving record stays clean.

Does being married lower my premium?

Not always, but many insurers offer small discounts because married drivers tend to file fewer claims.

Why do teen drivers cost more?

Teens are new to driving and statistically more likely to be involved in accidents, which increases their premiums.

Does switching insurers automatically save money?

Switching can save money, but not always. Every insurer prices risk differently. Always compare multiple quotes before switching.

Do safety features lower my premium?

Yes. Advanced safety features can reduce accident risk and theft likelihood, lowering your overall premium.

The Final Word On – How Much Is General Car Insurance

Understanding how much general car insurance costs helps you make informed decisions, choose appropriate coverage, and avoid paying more than necessary. While national averages offer a general idea of what most drivers pay, your personal premium depends on your driving history, location, vehicle type, credit profile, and coverage choices. Once you understand these factors, you can estimate your likely cost more accurately and take steps to reduce it.

The smartest approach when searching for the best general auto insurance plan is to compare quotes consistently, maintain a clean driving record, optimize your coverage, and take advantage of discounts. Doing so can help you learn exactly how much general car insurance is where you live. With the right strategy, you can secure reliable protection and save big, too. behind the wheel.

Compare general car insurance quotes online in 5 minutes. Save hundreds today on general auto insurance with direct rates.